Published: July 15, 2025 |

Updated: February 17, 2026 |

Reading Time: 22mins |

By: Sean Sullivan

In the complex world of warehouse management and logistics, few topics are as foundational yet frequently misunderstood as inventory valuation. For supply chain professionals, understanding how to properly value inventory isn’t just an accounting exercise—it’s a strategic capability that impacts everything from financial reporting to operational decision-making. Whether you’re managing a small warehouse or overseeing a complex distribution network, the method you choose to value your inventory can significantly affect your company’s profitability, tax obligations, and overall financial health. This comprehensive guide will explore the various inventory valuation methods, provide practical insights into their application, and address common challenges faced by logistics and supply chain professionals in today’s dynamic marketplace.

What is Inventory Valuation and Why is it Important?

Inventory valuation is the process of assigning monetary values to inventory items a company holds for sale. This seemingly straightforward concept becomes complex when considering the fluctuating costs of acquiring or producing these items over time. For warehouse and logistics managers, inventory valuation serves as the bridge between physical stock management and financial reporting, playing a crucial role in determining a company’s financial position. The significance of inventory valuation extends far beyond simple compliance with accounting standards; it directly influences key business metrics and decision-making processes. When inventory is properly valued, management gains accurate insights into cost structures, allowing for more informed pricing strategies and procurement decisions.

The impact of inventory valuation on profit margins cannot be overstated, as it directly affects the cost of goods sold (COGS) figure on income statements. A higher COGS results in lower gross profits, while a lower COGS yields higher gross profits—even when the physical inventory and sales remain unchanged. This accounting reality makes inventory valuation a powerful financial lever that can significantly impact a company’s profitability metrics and, consequently, its market valuation. Additionally, inventory valuation methods influence tax obligations, with different approaches potentially deferring or accelerating tax payments based on how they recognize inventory costs. For publicly traded companies, the chosen valuation method also affects financial ratios that investors and analysts use to evaluate company performance, such as inventory turnover rates and working capital metrics.

Furthermore, inventory valuation provides critical information for operational decision-making, helping warehouse managers identify slow-moving or obsolete items that tie up capital and storage space. This visibility enables more efficient inventory management practices, including optimized reorder points, improved warehouse space utilization, and reduced carrying costs. In industries with seasonal demand patterns or volatile commodity prices, the selected valuation method can either smooth out or amplify the financial impact of these fluctuations, affecting everything from budget planning to performance evaluation. Given these far-reaching implications, choosing the appropriate inventory valuation method represents a strategic decision that should align with a company’s broader financial and operational objectives.

Warehousing, accounting, purchasing, and order management—integrated software that grows with your business.

Request a Demo

Overview of Primary Inventory Valuation Methods

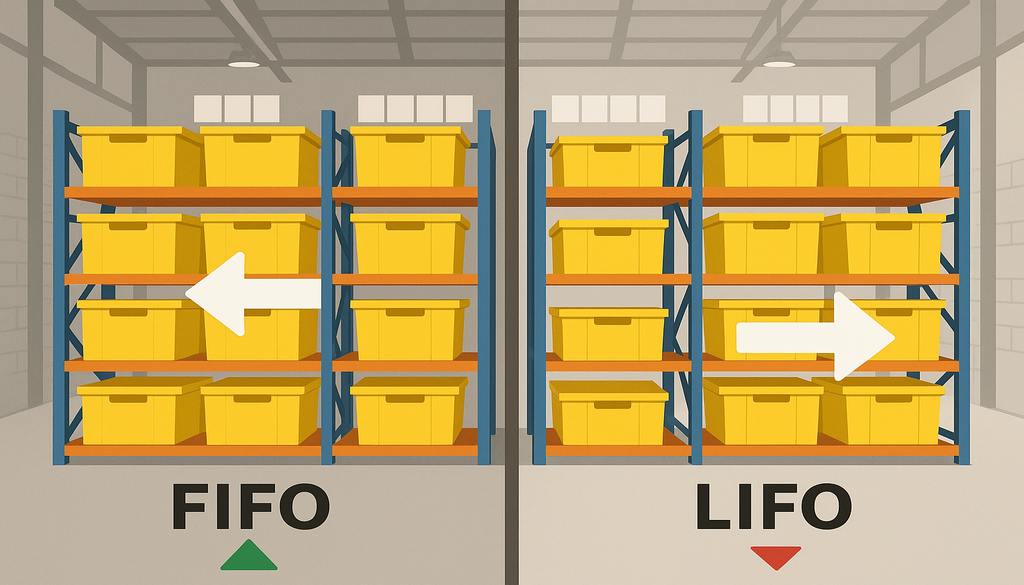

First-In, First-Out (FIFO) is one of the most widely used inventory valuation methods, operating on the logical assumption that the first items received in inventory are the first ones sold or used. This method closely mirrors the actual physical flow of goods in many warehouses, making it intuitively appealing for logistics professionals. Under FIFO, the cost of the oldest inventory items is assigned to the cost of goods sold, while the most recently acquired items remain in ending inventory. During periods of inflation, FIFO typically results in lower COGS and higher reported profits, as older, less expensive inventory items are expensed first. This approach provides a more current valuation of remaining inventory on the balance sheet, as ending inventory consists of the most recently purchased items at their actual acquisition costs.

Last-In, First-Out (LIFO), while less common globally due to restrictions under International Financial Reporting Standards (IFRS), remains a permissible method under U.S. Generally Accepted Accounting Principles (GAAP). LIFO operates on the opposite assumption from FIFO, assigning the cost of the most recently acquired inventory to COGS first. This approach often creates a tax advantage during inflationary periods, as the newest—and typically more expensive—inventory costs are matched against current revenues, reducing taxable income. However, LIFO can lead to outdated inventory valuation on the balance sheet, as the oldest costs remain assigned to the items in ending inventory. For warehouse managers, LIFO creates a disconnect between physical inventory flow and accounting records, potentially complicating physical inventory counts and reconciliations with financial statements.

Weighted Average Cost represents a middle ground between FIFO and LIFO, calculating a per-unit average cost by dividing the total cost of goods available for sale by the total units available. This method is particularly suitable for businesses dealing with homogeneous products or commodities where individual units are indistinguishable from one another. The weighted average approach smooths out price fluctuations and simplifies record-keeping, making it attractive for companies with high-volume inventory movements or those using perpetual inventory systems. For warehouse operations handling fungible goods like grains, chemicals, or bulk materials, weighted average cost aligns well with physical inventory management practices while reducing the accounting complexity associated with tracking individual lot costs.

Specific Identification, the most precise but also most labor-intensive method, tracks the actual cost of each specific item in inventory from acquisition through sale. This approach is typically reserved for high-value, uniquely identifiable items such as luxury goods, custom machinery, or rare collectibles. Advances in inventory management systems, particularly those utilizing RFID technology or serialized tracking, have made specific identification more feasible for a broader range of products. For logistics operations handling configured-to-order products, specialty items, or items with significant unit-to-unit cost variations, specific identification provides unparalleled accuracy in matching inventory costs to sales, though at the expense of increased tracking requirements and system complexity.

Comparing Inventory Valuation Methods: Pros and Cons

When evaluating FIFO, logistics professionals appreciate its alignment with natural inventory flow and operational reality—most warehouses aim to move older stock first to reduce spoilage and obsolescence. FIFO’s key advantage lies in its current and relevant ending inventory valuation, presenting a more accurate representation of replacement costs on the balance sheet. This method also typically produces more stable gross margin trends over time, making financial performance more predictable and easier to analyze. However, during inflationary periods, FIFO can create a tax disadvantage by reporting higher profits and consequently higher tax liabilities. Additionally, FIFO may not reflect the economic reality of certain industries where newer inventory might be sold before older stock due to customer preferences or specific handling requirements.

LIFO offers significant tax advantages during inflationary periods by matching current costs against current revenues, effectively reducing taxable income and improving cash flow in the short term. This method can better reflect economic reality for businesses where newer inventory is naturally sold before older stock, such as in coal mining or certain bulk material handling operations. However, LIFO’s disadvantages include potentially outdated inventory valuations on the balance sheet and the creation of “LIFO layers” that can complicate inventory tracking and financial analysis. International businesses face particular challenges with LIFO as it’s prohibited under IFRS, requiring companies to maintain separate inventory records for IFRS reporting. Furthermore, LIFO can distort financial ratios like inventory turnover and create issues during periods of significant inventory reduction, potentially triggering substantial one-time tax liabilities when old, low-cost LIFO layers are liquidated.

Weighted Average Cost provides computational simplicity and operational efficiency, especially for businesses dealing with homogeneous or commodity-type products where individual unit tracking is impractical. This method moderates the impact of price volatility, producing smoother earnings patterns compared to FIFO or LIFO during periods of fluctuating costs. For warehouse operations using automated inventory management systems or dealing with bulk materials stored in tanks or silos, weighted average aligns well with physical reality. The primary disadvantage, however, is that weighted average cost may not accurately reflect either the current market value of inventory or the specific historical cost of goods sold, potentially obscuring important pricing trends or cost patterns. Additionally, for businesses with significant price fluctuations or seasonal buying patterns, the averaging effect might mask important cost variations that could otherwise inform procurement or pricing decisions.

Specific Identification offers unparalleled accuracy in inventory valuation by tracking the actual cost of each individual item, making it ideal for high-value, unique, or customized products. This method provides the most precise matching of costs to revenues and gives management maximum control over profit margins through selective selling decisions. For logistics operations handling serialized products, specific identification enables detailed profitability analysis at the individual item level. However, this precision comes at a considerable cost in terms of tracking requirements, system complexity, and administrative overhead. Without robust inventory management systems and disciplined operational processes, specific identification can become prohibitively labor-intensive and error-prone. For high-volume operations or those dealing with physically indistinguishable goods, the additional tracking burden often outweighs the marginal benefits in valuation accuracy, making this method impractical for many warehouse environments.

When selecting an inventory valuation method, companies should consider their industry characteristics, product type, operational patterns, and strategic objectives. Businesses experiencing rapid inventory turnover with minimal price fluctuations might find FIFO or weighted average most suitable, while those facing significant inflation in input costs might benefit from LIFO’s tax advantages. Companies with diverse product lines might even employ different valuation methods for different inventory categories, optimizing the approach based on specific product characteristics and management objectives. Ultimately, the chosen method should align with both operational realities and financial reporting goals, providing meaningful information for decision-making while minimizing administrative burden.

Common Challenges in Inventory Valuation

Fluctuating market prices present one of the most persistent challenges in inventory valuation, particularly for businesses dealing with commodities or materials subject to volatile supply chain conditions. When procurement costs change rapidly, the chosen valuation method can significantly impact reported financial results, creating disconnects between physical inventory levels and their assigned values. For warehouse managers, these price fluctuations complicate budgeting, forecasting, and performance measurement, as cost variances may be attributed to valuation effects rather than operational efficiencies or inefficiencies. Businesses in industries with seasonal pricing patterns or those dependent on globally traded commodities face additional complexity, as their inventory values may fluctuate based on market forces entirely outside their control. Developing robust price trend analysis capabilities and implementing forward-looking procurement strategies become essential for managing this challenge effectively, allowing companies to make informed decisions about when to build inventory and when to draw it down based on anticipated price movements.

Obsolete and slow-moving inventory presents another significant valuation challenge, requiring companies to make difficult decisions about writing down inventory values below their original cost. For warehouse operations, identifying and addressing obsolescence is both an accounting necessity and an operational imperative, as outdated inventory consumes valuable storage space and ties up working capital. The subjective nature of determining when inventory has become obsolete or significantly decreased in value introduces complexity into the valuation process, often requiring cross-functional collaboration between accounting, operations, and sales teams. Businesses with products subject to technological advancement, fashion trends, or short shelf lives face particularly acute obsolescence risks, necessitating more frequent inventory reviews and more aggressive provisioning policies. Implementing systematic approaches to identify aging inventory, establishing clear criteria for obsolescence determination, and developing secondary market strategies for slow-moving items can help mitigate these challenges while ensuring inventory valuations remain realistic.

Regulatory and compliance hurdles add another layer of complexity to inventory valuation, particularly for multinational companies operating under different accounting frameworks. The divergence between tax reporting requirements and financial accounting standards often necessitates maintaining parallel inventory records, creating additional administrative burden and reconciliation challenges. Industries subject to specialized regulations, such as pharmaceuticals, food products, or hazardous materials, face additional compliance requirements that may influence how inventory is valued and reported. For publicly traded companies, the increased scrutiny from auditors, regulators, and investors regarding inventory valuation methodologies and assumptions adds pressure to ensure valuation approaches are defensible and consistently applied. Staying abreast of changing regulations, investing in compliance training for inventory management personnel, and implementing robust documentation processes become essential for navigating these regulatory challenges effectively.

Technical limitations in inventory management systems can further complicate accurate valuation, particularly when legacy systems lack the capability to support sophisticated tracking methods or integrate with financial reporting tools. Many warehouses struggle with real-time inventory visibility, making it difficult to reconcile physical counts with system records and leading to valuation discrepancies. The integration gap between operational warehouse management systems and financial accounting platforms often requires manual interventions and adjustments, introducing error potential and delaying financial close processes. For companies transitioning to new inventory management technologies or expanding operations across multiple locations, maintaining consistent valuation methodologies across different systems adds another layer of complexity. Investing in integrated technology solutions that bridge operational and financial requirements, implementing robust data governance practices, and establishing clear procedures for system updates and reconciliations can help address these technical challenges while improving overall inventory valuation accuracy.

Best Practices for Accurate Inventory Valuation

Regular audits and accurate record-keeping form the foundation of reliable inventory valuation, providing the factual basis upon which all valuation methodologies depend. Implementing a structured cycle counting program rather than relying solely on annual physical inventories allows for ongoing verification of inventory accuracy without disrupting warehouse operations. This approach enables prompt identification and correction of discrepancies, preventing small errors from accumulating into significant valuation issues. For effective inventory records, warehouse managers should establish clear documentation standards for all inventory movements, including receipts, transfers, returns, and adjustments. These standards should include required information fields, approval workflows, and timeframes for recording transactions. Developing a robust audit trail that tracks changes to inventory records, including who made changes and why, enhances accountability and simplifies troubleshooting when discrepancies arise. Additionally, implementing segregation of duties between physical custody of inventory and record-keeping functions reduces fraud risk while improving overall control effectiveness.

Leveraging technology for real-time inventory tracking represents a significant opportunity to enhance valuation accuracy while simultaneously improving operational efficiency. Modern warehouse management systems with integrated barcode scanning, RFID capabilities, or IoT sensors can dramatically reduce manual counting errors and provide near-instantaneous visibility into inventory movements. When connected to enterprise resource planning (ERP) systems, these technologies enable automated cost calculations based on the chosen valuation method, eliminating error-prone manual calculations and ensuring consistent application of accounting policies. Advanced analytics capabilities within these systems can identify patterns indicative of potential valuation issues, such as unusual cost fluctuations or reconciliation discrepancies, allowing for proactive investigation. Cloud-based inventory management solutions further enhance accuracy by enabling real-time updates across multiple locations, ensuring all stakeholders work with current information. For companies managing complex supply chains, blockchain technology offers promising capabilities for creating immutable, transparent records of inventory movements and their associated costs, potentially revolutionizing inventory valuation practices.

Training and development for inventory management teams remains crucial yet often overlooked in the pursuit of valuation accuracy. Warehouse personnel need to understand not only the operational aspects of inventory management but also the financial implications of their activities. Comprehensive training programs should cover the basics of the company’s chosen valuation methodology, the importance of accurate and timely transaction recording, and the potential impact of errors on financial reporting. Cross-functional training sessions involving both operations and finance staff can help build mutual understanding of challenges and requirements, fostering collaborative problem-solving approaches. Regular refresher training addressing common error patterns identified through audits or system reports helps reinforce best practices and address emerging issues. For management-level staff, more advanced training on inventory analytics, valuation strategy, and regulatory requirements enables more informed decision-making and better oversight of valuation processes.

Establishing clear policies and procedures specifically addressing inventory valuation creates a structured framework for consistent application across the organization. These policies should document the selected valuation method(s), criteria for making valuation adjustments (such as for obsolescence or damage), required approval levels for write-downs, and reconciliation procedures between physical counts and system records. For companies operating multiple warehouses or distribution centers, standardized procedures ensure consistent application of valuation principles across locations, simplifying consolidation and financial reporting. Implementing formal change management processes for inventory valuation policies helps ensure that any modifications are properly vetted, documented, and communicated throughout the organization. Regular policy reviews by cross-functional teams including operations, finance, and compliance personnel help identify improvement opportunities and ensure alignment with evolving business needs and regulatory requirements. By creating this structured governance framework, companies can significantly enhance the reliability and defensibility of their inventory valuations while reducing the risk of material misstatements in financial reporting.

The Future of Inventory Valuation in Warehouse Management

Emerging trends are reshaping inventory valuation strategies across the supply chain industry, driven by changing business models and market expectations. The growing adoption of just-in-time inventory practices and lean manufacturing principles has reduced overall inventory levels, making accurate valuation of remaining stock even more critical. Simultaneously, the rise of omnichannel retail and distributed fulfillment networks has complicated inventory tracking, as products flow through multiple channels and locations before reaching customers. These complex fulfillment patterns create new challenges for traditional valuation methods, particularly when determining which inventory costs should be assigned to which sales channels. The increasing focus on sustainability and environmental accounting is also influencing inventory valuation, with companies beginning to incorporate carbon footprint considerations and environmental compliance costs into their inventory value assessments. Forward-thinking organizations are exploring methodologies that account for these externalities, potentially changing how inventory costs are calculated and allocated.

Artificial intelligence and machine learning represent transformative forces in inventory valuation, offering capabilities that extend far beyond traditional accounting approaches. AI-powered systems can analyze historical data patterns to predict obsolescence risks, allowing for more proactive provisioning and more accurate valuation adjustments. Machine learning algorithms can identify subtle correlations between product characteristics, market conditions, and inventory movement patterns, enabling more precise forecasting of inventory values under different scenarios. These technologies are particularly valuable for businesses with complex, diverse inventory portfolios, where manual analysis would be prohibitively time-consuming. Predictive analytics tools can simulate the financial impact of different valuation methodologies under various market conditions, helping companies select the optimal approach for their specific circumstances. As these technologies mature, they promise to shift inventory valuation from a retrospective accounting exercise to a forward-looking strategic capability that provides real-time insights for decision-making.

The integration of operational and financial systems continues to evolve, breaking down traditional silos between warehouse management and accounting functions. This convergence enables real-time financial visibility into inventory movements, with valuation calculations performed automatically as transactions occur rather than as period-end adjustments. The development of unified data platforms that serve both operational and financial needs eliminates reconciliation requirements and reduces the risk of inconsistencies between systems. These integrated solutions are increasingly incorporating advanced visualization tools that make inventory valuation insights accessible to non-financial managers, improving cross-functional collaboration and decision-making. For global organizations, these unified platforms can simultaneously apply different valuation methodologies for different reporting requirements (such as GAAP vs. IFRS), maintaining consistency while meeting diverse compliance needs. This integration trend represents a significant advancement toward the goal of “single source of truth” information systems that support both day-to-day operations and financial reporting requirements.

Blockchain technology and distributed ledger systems offer particularly promising applications for inventory valuation, potentially providing unprecedented transparency and traceability throughout the supply chain. By creating immutable records of every transaction affecting inventory, blockchain can establish indisputable audit trails that simplify verification and reduce disputes about inventory costs. Smart contracts built on blockchain platforms could automate valuation adjustments based on predefined criteria, such as aging thresholds or market price changes, ensuring consistent application of policies without manual intervention. For companies with complex international supply chains, blockchain can provide reliable provenance information and cost tracking across multiple parties and jurisdictions, addressing one of the most challenging aspects of inventory valuation. While still emerging, these blockchain applications represent a potential paradigm shift in how inventory movements and their associated costs are recorded, verified, and reported, offering a glimpse into a future where inventory valuation becomes more transparent, automated, and trustworthy.

Conclusion

Inventory valuation stands as a critical function that bridges warehouse operations and financial management, influencing everything from tax obligations to strategic decision-making. Through this comprehensive exploration, we’ve examined the primary valuation methodologies—FIFO, LIFO, weighted average cost, and specific identification—each offering distinct advantages and limitations depending on business circumstances and objectives. We’ve also addressed the common challenges faced by logistics professionals, from fluctuating market prices to obsolescence issues, while providing practical strategies for enhancing valuation accuracy and reliability. As technology continues to advance, the future of inventory valuation promises greater automation, integration, and analytical sophistication, enabling more strategic approaches to inventory management.

For warehouse and supply chain professionals, the key takeaway remains that inventory valuation is not merely an accounting exercise but a fundamental business process with far-reaching operational implications. By understanding the principles, challenges, and best practices discussed in this article, logistics managers can make more informed decisions about their inventory valuation approaches, better collaborate with financial teams, and ultimately contribute more effectively to their organization’s success. Moving forward, companies that view inventory valuation as a strategic capability rather than a compliance requirement will gain competitive advantage through more accurate financial reporting, improved decision-making, and more efficient capital utilization.

Frequently Asked Questions (FAQ)

How does inventory valuation affect financial reporting?

Inventory valuation significantly impacts financial reporting by directly affecting both the balance sheet and income statement. On the balance sheet, it determines the value of inventory assets reported, influencing key financial ratios like current ratio and working capital. On the income statement, inventory valuation methods determine the cost of goods sold (COGS), which directly impacts gross profit, operating income, and net income. Different valuation methods can produce substantially different financial results, even when the physical inventory and sales remain identical. For publicly traded companies, these effects can influence investor perceptions, stock valuations, and compliance with debt covenants, making inventory valuation a critical component of financial reporting integrity.

Which inventory valuation method is best for tax purposes?

For tax purposes, LIFO (Last-In, First-Out) often provides the greatest advantage during inflationary periods by matching newer, higher-cost inventory against current revenues, resulting in higher COGS and lower taxable income. This tax deferral benefit can significantly improve cash flow, though companies must use the same method for financial reporting as they do for tax reporting. However, the optimal method varies based on specific business circumstances, inflation rates, and regulatory environments. Companies operating internationally should note that LIFO is prohibited under IFRS, creating potential complications for global operations. Before selecting a method for tax purposes, businesses should consult with tax professionals to evaluate long-term implications, including potential tax liabilities that might arise from future inventory reductions or method changes.

How can technology improve inventory valuation processes?

Technology significantly improves inventory valuation through automated data capture and real-time updates. Barcode scanning and RFID systems eliminate manual counting errors while providing instant inventory visibility. Integrated ERP and warehouse management systems automatically calculate values using chosen methodologies and connect physical movements directly to financial records, eliminating reconciliation issues. AI algorithms can predict obsolescence risks and identify valuation anomalies, while these technologies collectively reduce labor costs and accelerate financial reporting cycles.

What are the risks of using the LIFO method during deflationary periods?

During deflationary periods, LIFO expenses newer, lower-cost inventory first, resulting in higher taxable income and increased tax liabilities despite challenging economic conditions. This creates artificially inflated inventory values that may mislead stakeholders about true asset replacement costs. Additionally, reducing inventory levels can trigger liquidation of older, higher-cost LIFO layers, causing substantial one-time income spikes and unexpected tax burdens.

Can inventory valuation methods impact investment decisions?

Yes, inventory valuation methods directly impact investment decisions by affecting key financial metrics that investors use to evaluate companies. Different methods can significantly alter reported profitability, asset values, and financial ratios, even when business operations remain unchanged. Sophisticated investors analyze these policies to make appropriate comparisons between companies. Additionally, unexplained changes in inventory valuation methods can raise red flags about financial management practices, potentially affecting investor confidence and company valuations.

Essential Cannabis Warehouse Management Strategies

Discover effective cannabis warehouse management with key inventory strategies and software solutions. Optimize your operations today!

Third-Party Logistics Services: Your Complete Guide

Discover how 3PL services can transform your logistics strategy. Learn about warehouse and logistics services, top companies, and future trends.

3PL Logistics Explained: Services, Models, and Benefits

Discover how 3PL logistics can transform your supply chain with our comprehensive guide.